Value creation …

The evolution of Carrefour's economic profitability

By Dominique Jacquet

When, on February 18, Carrefour presented its 2020 annual accounts, the market observed that the improvement in economic and financial profitability, which began in 2018, was continuing: significant improvement in operating income and free cash flow, debt reduction, announcement of the resumption of the dividend paid in cash and not in securities.

A quick calculation shows that the return on capital employed (the famous ROCE) now exceeds 15%, up 3% compared to 2017.

The price reacted strongly to this announcement by closing at € 14.57, a decrease of 4 Euro cents compared to the previous day… It was around € 16 3 years ago.

Carrefour’s enterprise value (EV = market capitalization + financial debt net of cash) is ultimately identical to the book capital employed and the firm neither generates nor destroys value.

However, a pre-tax ROCE of 15% deserves more favorable treatment. The so-called Market-To-Book ratio is obtained by dividing the enterprise value by the book capital employed: MTB = EV / CE. If the MTB is greater than unity, there is value creation, otherwise destruction.

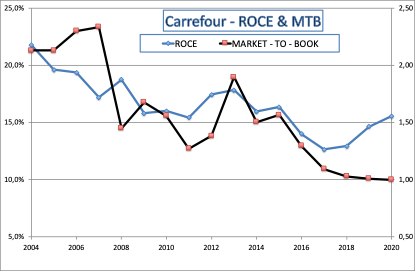

Here is the correlation between ROCE and MTB for Carrefour over more than 15 years.

This graph reminds us that value creation comes from financial performance!

However, we demonstrate that this ratio, in the absence of growth, is theoretically equal to the ratio of after-tax ROCE divided by the cost of capital. Carrefour’s cost of capital is probably between 5% and 6% and the group would therefore deserve a MTB of 1.5 or 2, more under a growth assumption …

This gap between market value and “earned” value is called a credibility gap, already mentioned in these lines. It appears when a company is entering a strategic shift or is recovering after a difficult period, the latter case being a good description of Carrefour’s situation.

We have never seen a credibility gap “close” in less than 4 years, but sometimes it takes longer for the market to be convinced of the sustainability of the recovery. However, it only appeared 3 years ago … Patience?

If there is one person who is already convinced of the return to sustainable performance today, it is Alain Bouchard, founder and owner of Alimentation Couche-Tard, a Canadian company which, on January 12, offered € 20 per share for take control of Carrefour. The price rose modestly to € 18 during the session to drop to € 15, the French authorities immediately opposing the merger.

This is called a “credibility gap extension” …