Danone, what’s next ?

Did 2 years of intense and relevant post-activism improve the financials?

By Ivan Cuesta

(special collaboration)

(Illustration created for this blog through Artificial Intelligence, with the help of Adobe Firefly)

In January and February 2021, Danone faced two activist events from Bluebell Capital and Artisan Partners. Both hedge funds challenged the financial performances and the governance of the company. Consequently, the CEO and Chairman Emmanuel Faber was sacked, and the Board of Directors initiated a complete renewal. What about financial performance? Did the activist’s events provoke a positive financial outcome?

To answer the question, we will look at the financial KPIs, ROA, Tobin’s Q, and abnormal stock returns, as they are the most significantly used by financial economists for firms’ performances regarding activist events.

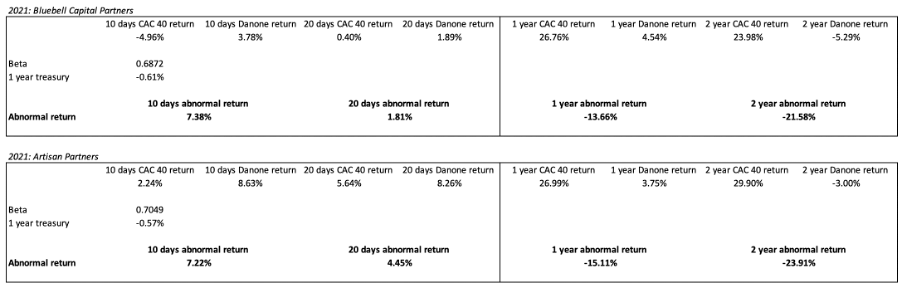

Abnormal Returns

The abnormal return is calculated as follows: Actual return – Expected return.

The expected return follows the capital asset pricing model (CAPM), which is defined as follows: Expected return = Risk-free rate + beta x (expected market return – risk-free rate).

Figure 1: Danone Abnormal returns, from Eikon from Thomson Reuters.

In Figure 1, we can observe positive abnormal returns in the short term, in both activists’ events, 10 days and 20 days after Danone has been targeted. After 1 year of the activists’ events, there is a significant negative impact as it shows respectively -13.66% and -15.11% abnormal returns for the Bluebell Capital and Artisan Partners events. After 2 years, we observe a further negative impact with -21.58% and -23.91%, respectively.

If we compare with Nestle (Figure 2), after its activist event in 2017, we can observe important gaps of abnormal returns in favour of Nestle compared to Danone.

Figure 2: Nestle Abnormal returns, from Eikon from Thomson Reuters.

The comparison with Unilever, with the event of Nelson Peltz in January 2022, also shows a much better performance versus Danone for the 1-year abnormal return (Figure 3).

So it is clear that the 2021 activists’ events did not create a positive momentum for Danone in terms of abnormal returns, and the comparison to peers which faced also activists highlights even more the bad performance of French yogurt maker.

Figure 3: Unilever Abnormal returns, from Eikon from Thomson Reuters.

ROA

To look at the potential effect on the ROA, we performed an analysis to evaluate the correlation between the activist event and the ROA performance. The weighing of the activist’s power of influence has been estimated between 0 to 1 during the period. The correlation in Figure 4 shows a value of (0.62), which demonstrates a negative correlation between the activists’ events and the development of ROA. The activists’ events did not create a positive outcome in terms of ROA so far.

Figure 4: Danone Return on Assets, from Annual Reports.

As a comparison in Figure 5, Nestle demonstrates a positive development of ROA with the activist event held in 2017.

Figure 5: Nestle Return on Assets, from Annual Reports.

As per the abnormal return, Danone shows negative performances in terms of ROA and the comparison to Nestle confirms the trend.

Tobin’s Q

Tobin’s Q is defined as the enterprise value divided by the capital employed. Enterprise value is the sum of the market capitalization and the net debt.

Figure 6: Danone Tobin’s Q, from Annual Reports.

As per the ROA, we have applied the same coefficients of activists’ power of influence (Figure 5). We can also observe a negative correlation (-0.45) between the activists’ events and Tobin’s Q performances. This means the activists did not provoke positive outcomes for Tobin’s Q development.

We observe a different outcome compared with Nestle’s performances in Figure 6. In this case, a positive correlation exists between the activist’s event in 2017 and Tobin’s Q evolution.

This last KPI and comparison to Nestle, confirm the fact that despite the activists’ pressure of 2021, Danone is consistently under performing and that the trend is not changing so far.

Figure 7: Nestle Tobin’s Q, from Annual Reports.

Did the activists do a good job?

Artisan Partners and Bluebell Capital’s reputation is highly credible and has proven track records, being part of the Top 100 Asset Management firms in the world and part of the Top 25 activist investors (Eikon Thomson Reuters). The credibility of Artisan Partners was even reinforced by the support of the “golden leash” Jan Bennink for the activist‘s targeting of Danone. In terms of intensity, the very active public communication of both activists requesting drastic changes, and the governance revolution they managed to obtain in 3 months from the Bluebell Capital’s attack, have shown that the intensity required to provoke changes was high enough.

Therefore, we can acknowledge that both activist’s events in 2021 were appropriate to induce a positive momentum in terms of financial performance, but there was no positive outcome, both on stock and economic performances, especially compared with Nestle and Unilever.

Conclusion

The probability that an activist event provokes positive financial outcomes depends on two parameters from the activist’s side: the activist’s reputation and the intensity of the attack.

Despite the relevance of the activists’ attacks in 2021 and their governance consequences, the financial performances of Danone did not match the expectations in terms of improvement and benchmark. We can then subscribe to the uselessness of activism to transform Danone into a performer reference. As the company faced two more activists attacks previous to 2021, in 2012 and 2017, without financial impacts, we can design two future scenarios for the following months: either the company will be targeted again, with an even more aggressive approach by an activist, or the company will be subject to a hostile takeover. After 10 years of underperformance, there is no other way to see the light out of the tunnel.