Back to growth !

Facebook's trajectory is full of twists and turns...

By Dominique Jacquet

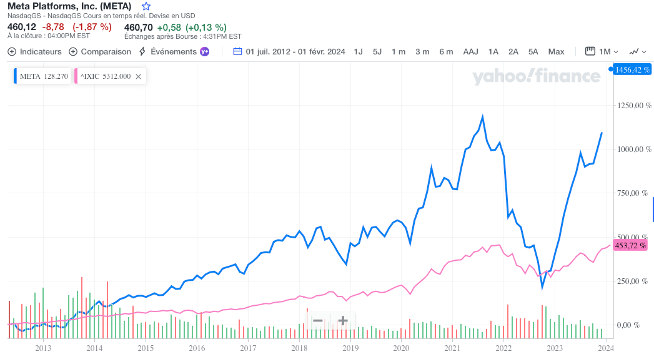

The stock market trajectory of META (Facebook) is not lacking in twists and turns… After a rather disastrous IPO, the price experienced growth well above the Nasdaq for 9 years before collapsing in 2022, losing three-quarters of its value between August 2021 and October 2022, then to experience a spectacular rise, returning to its highest levels at the time of publication of the accounts in early February 2024.

If the year 2022 was penalized by questions about the firm’s growth capacity, the results for 2023, quarter after quarter, showed that META retained significant growth options. The number of users is clearly stagnating in North America and Europe, but ARPU (Average Revenue Per User) has resumed its progression after having stagnated or slightly decreased in 2022: for North America, from $60 in 2021 to $59 in 2022, but $68 in 2023. Asia and the Rest of the World welcome the largest battalions of users with, in total, 2.4 billion monthly users, an increase of around 100 million users compared to 2022. Certainly, the ARPU is much lower with an average of $5 per user, but up by almost $1 compared to the previous year and with good growth prospects. As the company focused the year 2023 on productivity (22% reduction in personnel), increasing, among other things, the gross margin by 2.5% and gaining 4% on commercial costs, the operating result has increased by 10% and represents 35% of revenues. The ROCE followed, increasing from 26% to 37% and the share price increased by 25% in one session!

As the cash generated by operations has largely outweighed investments (Capex and acquisitions) for several years, META began to return cash to shareholders in 2017 through share buybacks with a peak at 44.5 billion dollars in 2021. Nearly 20 billion in 2023 and the authorization to again purchase more than 80 billion dollars of shares in the firm. Concretely, the company still has more than 65 billion in the bank with a financial debt of less than 20 billion.

The massive share buybacks of 2021 did not prevent the price from collapsing in 2022. Indeed, this financial operation can be interpreted by investors as a signal of undervaluation of the firm (positive signal) or, on the contrary, the confession of the absence of growth opportunities (negative signal). The second interpretation prevailed.

However, by announcing the 2023 results, META reiterated its share buyback objective, but added very important news: for the first time in its existence, the company will pay a dividend of $0.5 per quarter, i.e. $2 per year. In terms of cash flow, the impact is limited. With 2.2 billion shares outstanding, the dividend represents a cash outflow of $4.4 billion, well below the amounts invested in share buybacks. On the other hand, the very nature of the payment of a dividend has an impact on the signal sent to the market. The buyback of shares is an operation that can be modulated or interrupted at any time, which gives it a characteristic of non-predictability. On the other hand, a dividend represents an announcement of future flows which, barring an accident, will grow, year after year. For a pension fund, META is no longer a firm that returns its performance by reducing its number of shareholders, it is a financial asset generating predictable incoming flows which can easily constitute a sort of secured-dividend “portfolio base”, as telecommunications operators were at one time. The modest level of the dividend suggests that it can only increase given the firm’s performance. On the other hand, it is clear that companies that initiate a distribution of their net income send investors a message that is similar to the end of growth, which could be interpreted in a negative way.

When Microsoft announced in 2004 that the firm was going to pay an exceptional dividend ($36 billion…), buy back its shares and pay a recurring dividend, the market turned pale, concluding that the golden age and growth had come to an end ( prediction which turned out to be a little quick for a corporation which recently became the largest worldwide capitalization…). On the other hand, when Apple announced that after a period where the dividend had been eliminated, the company was going to distribute a dividend again to its shareholders, but of a very symbolic amount, the market did not move because the mobilized flows were negligible compared to the firm’s cash flow and free cash flow.

By giving a warm welcome to META’s announcements, including the dividend of $0.5 per quarter, the market gave more importance to the evolution of ARPU and the number of users in emerging countries than in modest distributive return to shareholders. However, it will be interesting to observe the (possible) future impact of this new distribution policy on META’s stock market status by drawing up a list of investors, their nature and their respective participation.

To conclude, let us recall the conclusion of the major article by Fisher Black (“The Dividend Puzzle”, Journal of Portfolio Management, 1976) which asked the existential question: “What should the corporation do about dividend policy? We don’t know.” Beautiful modesty from such a brilliant mind!