A million miles away…

Another failure for Intuitive Machines

By Dominique Jacquet

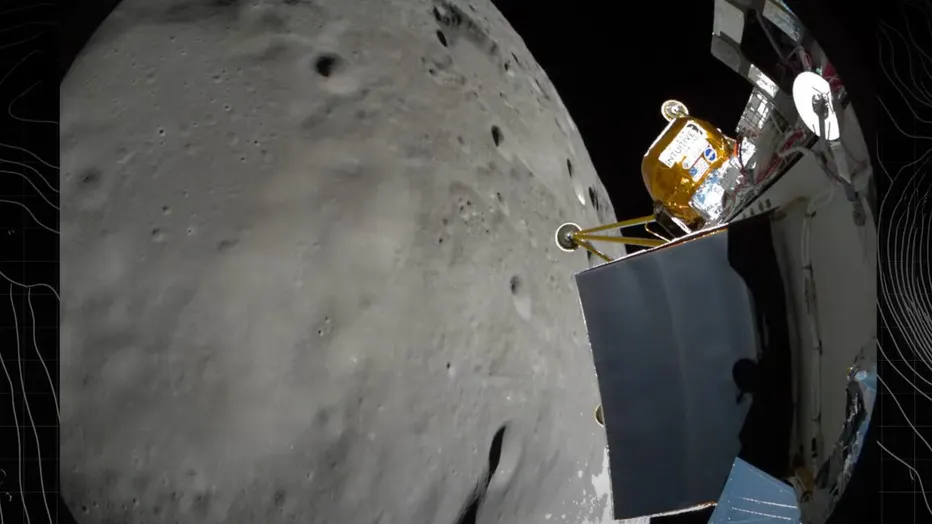

On March 6, Intuitive Machines’ second moon landing mission ended in a (new) partial failure.

The Moon’s south pole is both a major strategic issue and a considerable technical difficulty. To hope to find water (a source of energy) and locate it, you need to know where and how to drill in conditions of extreme and highly variable temperatures. This was the main mission of the equipment. To achieve this goal, the batteries of the equipment must be recharged, a delicate task because this area only knows a low sun.

The module landed near the target, but in a chaotic location and it ended up on its side, unable to deploy its solar panels, so quickly out of power: end of the mission.

As a predictable and immediate consequence, the stock price has lost nearly two-thirds of its value, from $20 to $7… The company’s market cap today stands at around $640M. Admittedly, the firm still has $385M in cash and only consumes about $80M each year, but NASA has put other firms, such as Astrobotic, Firefly Aerospace or Draper, in competition.

Intuitive Machines’ core value is, in theory, equal to the probability of being the operator ultimately selected by NASA multiplied by the firm’s ability to generate cash flows in the long run.

In a “portfolio” logic, the rational investor must put different eggs in the same basket corresponding to all the competitors working with the same objective. This is a problem when they are not listed on the stock exchange. The most well-known space operator, SpaceX, only “reveals” its “fundamental value” when raising funds or selling shares on the secondary market. Thus, we learn (source: Crunchbase) that this type of transactions were carried out in February 2024 on a valuation basis of $127bn, in June at the level of $210bn and in December by reaching $350bn. The problems encountered by Starship Flight 8, quite similar to the difficulties of issue 7, do not seem to have the same impact as for Intuitive Machines.

SpaceX is said to generate $13bn in revenue in 2024 thanks, for the most part, to 138 rocket launches ($4.2bn in revenue) and the commercialization of the famous Starlink network ($7.8bn).

These two examples lead us to questions about value.

A transaction is the consequence of a confrontation between supply and demand. The buyer anticipates a return on investment in the form of dividends and capital gains.

One of the acquirers of SpaceX shares in December 2024 is a small fund (worth $300M), which has lost approximately 20% of its value since the transaction and has just increased its stake. Its main shareholder is a small fund (assets under management of around $200M) which has underperformed the Nasdaq with great regularity for 5 quarters. Wouldn’t it have been better to choose a large firm to carry out the transactions in order to give more credibility to the valuation?

The Intuitive Machines evaluation is a combination of the portfolio approach (all competitors) and the economy of extremes (infinite market depth?). The analogy is strong with the evaluation (and management) of a high-risk R&D project, a subject that leaves financial theory and practice a little perplexed.

The uncertain evolution of a world in which companies seek to develop must lead the profession of evaluator to deepen and renew its practices.